Sunday, February 20, 2011

What is a Commercial Signal Failure

This is in response to a special request from my pal the Turd who has asked me if I would take a bit of time to explain the titled term. It dovetails nicely with my comments on the impact of margin requirement hikes by the exchanges.

Let me begin this explanation by saying that these events are relatively rare. Over the course of my career I can probably count the number of times that I have seen them occur on both hands. That is not to say that there have not been more, but in the particular markets that I actively trade, they are infrequent. However, when they do occur, the resultant price moves are spectacular; i.e. if you happen to be on the correct side. If you are not - well - you are probably no longer reading posts or having anything else to do with commodity futures markets and are gainfully employed elsewhere having had your net worth reduced by multiples.

Let's also take a Commercial Signal Failure (hereafter referred to as CSF) in a bull market. I have seen one occur in the hog market twice in my career and those were strong bear moves that resulted from chicken import bans and H1N1 outbreaks but for the most part, these things happen in a bull market.

Here is the scenario - a market begins a trending move higher. Speculators are on the long side driving the price upward with the Commercials (producers, processors, etc.) instituting hedges for risk management and selling into the speculator buying. This is all healthy and normal for the Commercials are using the futures markets for the reason that they came into being - they are locking in profit margins and eliminating price risk by transferring that risk to a speculator who is willing to assume the risk in the hopes of making money as prices move higher. It is also the reason that all bull markets that have any lasting power will always see a rise in open interest as price moves higher. Commercials are employing scale up selling programs to lock in successively higher sales prices for their production. This can be abused as it has been in gold and silver but that is another story that we all know too well.

As the price continues to move higher, commercials will attempt to take advantage of the speculative buying and will sell more and more of their expected future production. In other words, the size of their short position continues to grow as they cover their risk management needs. Now in order to maintain this short position, they are required like anyone else who has a position in the futures market to post margin. Bona fide hedgers have a distinct advantage in this however since the margin requirements for a hedger are less than that required by a speculator to post. In other words, they can control more contracts for the same amount of money than can a speculator.

The reason for this is because supposedly there is less risk for a hedger from a financial standpoint because they actually produce the commodity that they are hedging. If they lose money on the hedge, the short position, that is offset by the corresponding rise in the physical commodity. This conceivably puts them on a sounder financial footing than a speculator who is putting risk money up without having access to the underlying physical.

So far the scenario is developing like it does in every single bull market - the price rises, the speculators are on the long side, the commercials are on the short side, and the total open interest (number of contracts open) is rising. Obviously the speculators are now showing good open or paper profits on their long positions with the commercials showing paper losses on their open short positions. As price continues to rise, these commercials will also be required to post additional margin money to bring their positions back to what is called the maintenance level. The higher the price rises, the more money they must expend to meet all the clearinghouse requirements. That however is generally not a problem since these things are accounted for in their risk management programs and they have access to lines of credit which will allow them to make good on these financial requirements.

A problem develops for them however when there is an event, an occurence or development of some sort which drastically changes the supply/demand picture overnight. For example, a hard freeze could crush the Florida orange crop; a severe drought or flood could wipe out a substantial portion of a major agricultural crop, a livestock disease could surface in a major producing nation, a blight could strike the cocoa producing areas of West Africa, it could nearly anything. Whatever the event, it triggers an immediate shift in that fundamental supply and demand equation that results in a huge imbalance between demand and supply in favor of the speculators. In other words, supply has been severely impacted and sharply reduced or demand has shot up suddenly and is now grossly overwhelming supply. The result - prices spike rapidly upward and begin to accelerate higher as the market must now come to terms with the new and greatly alterated supply/demand equilibrium.

Commercials, who now find themselves on the short side of the market with a substantial position are suddenly caught flatfooted as panic buying grips the market and all offers to sell instantly disappear. The result is a massive air pocket above the market with a huge imbalance of buyers and sellers. Simply put - there are no sellers, anywhere. Everyone wants to buy and they have no one to buy from. What happens? Price must rise higher and higher until it reaches a level where the sellers, those who actually have the product, feel comfortable letting some of their supply go.

Some might say, well, what is the big deal for those commercials? After all, they have the product and while they are losing money on their short hedges, they are making it back on the physical side of thing because they actually produce the commodity. That is true and in a normal bull market, that is exactly what happens, but in a situation as above, where the event has come out of nowhere and was not anticipated and is of such magnitude that it severely throws the balance between supply/demand grossly out of balance, even these commercials are impacted.

Why is this? The answer goes back to the margin requirements. In a rising market, commercial hedgers with short positions are constantly losing money on those hedges and are required to post additional sums of money to keep current and maintain those short positions. As stated previously, to do this they draw from their own reserves which are set aside for risk management purposes. In addition they have lines of credit from various lenders who loan them the money for such purposes. But when an event alters the market dynamics to such an extent that price begins to gap higher and accelerates upward, their lines of credit are no longer sufficient to cover the paper losses on their open short positions.

In other words, they run into the exact same position as a speculator who has a market moving against him and no longer has the financial resources to maintain his margin deposit at the proper level. They are forced to get out of their positions because they have run out of money to maintain them. Unable to get any further credit and having drawn down their own reserves, they are now defenseless and must buy back the existing shorts to prevent the financial ruin of their firm.

They too now enter the buying frenzy only this time, their ability to get out of their shorts determines whether or not their firm will survive. They will hit every single available offer to sell that might appear because their very life depends on getting out. They do not care what the cost is - they must get out.

The implications are obvious - price will rise and rise and rise until every last one of those losing short positions have been cleaned out to the level that enables that firm to survive. As to how high that market will then go, it is anyone's guess. Quite frankly no one knows. It will stop at some point but by then the damage to the shorts is staggering.

Over the years I have seen entire firms go down when an event such as this transpired.

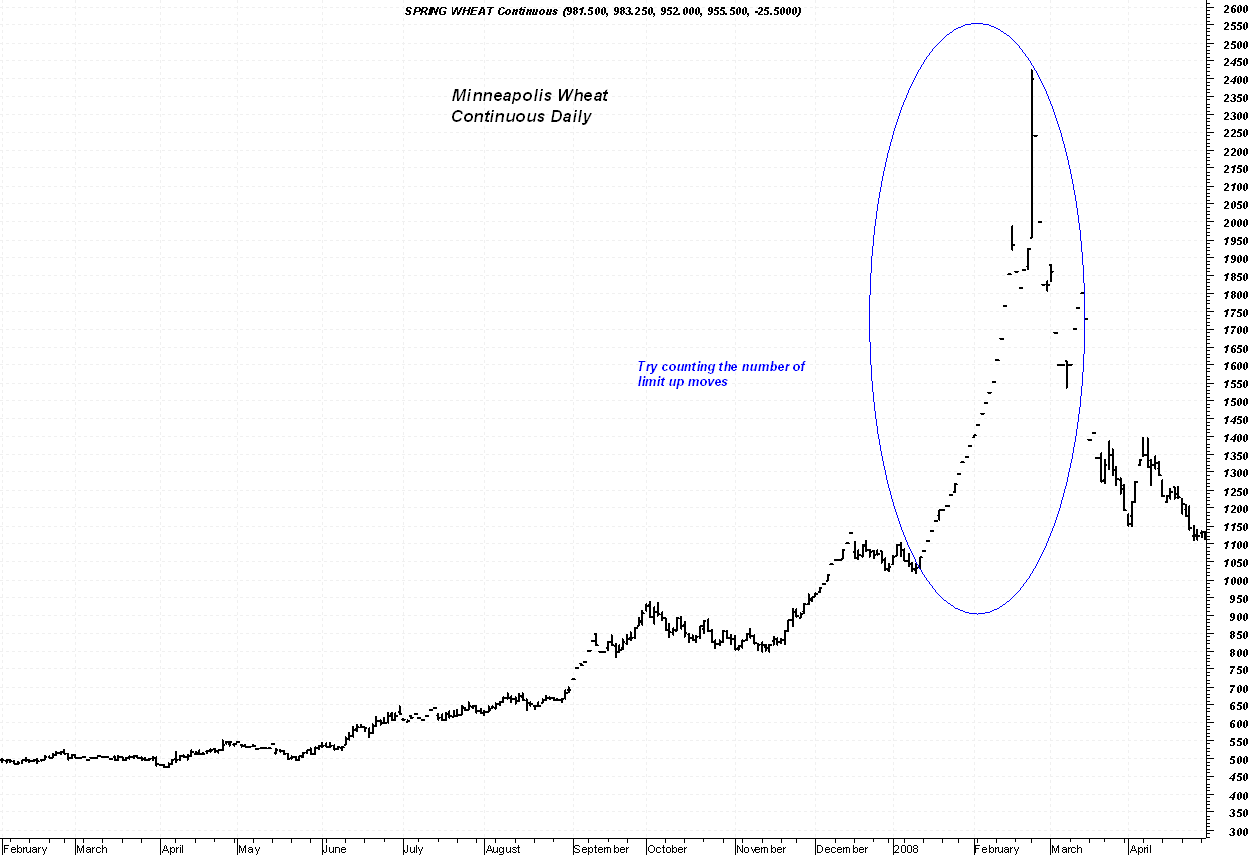

Here are a few charts detailing the results of a CSF. The first is in Live Cattle and the second is in Minneapolis Wheat.

With Live Cattle, the "black swan" event was the discovery of a cow in Canada back in 2003 that came down with "mad cow" disease resulting in the US authorities closing the border to all shipments of Canadian beef and live cattle. The result was an immediate shift in the supply/demand balance with US supply sharply curtailed and unable to meet the then existing demand. Price shot sharply higher moving limit up 8 days in a row, 5 of those days being gaps in which the market basically shut down because there was no one to sell.

I can still remember the cries and pleas from the commercials who were members of the CME for the exchange to do something because they could not get out and were being ruined.

The Minneapolis Wheat market, back in the winter of 2008, was roiled by a perfect storm of developments that seemed to come together all at once. Horrific crop weather, soaring demand, export bans from wheat growing countries, it just all hit at once. The result was the most spectacular Commercial Signal Failure that I have ever seen. Price soared from an already expensive $10.00/bushel to nearly $24.50 for a single bushel of this wheat! The market literally did not trade for days on end as it opened at limit bid day after day with absolutely no one to sell. There were more than a few firms who were destroyed as a result of their short hedges in this market.

I do want to point out something about these CSF's. Note that once they run their course, the market generally collapses and gives back a very large percentage of its overall gains. That is because once all the Commercials have finished buying back their bleeding short positions, there is no one left to buy and prices now come tumbling back to earth. In some cases, all the price rise is erased; in other cases a substantial portion are given back but the market then finds a footing at a new and higher price level.

As with any market, the potential always exists for such a development especially when there exists a very large short contingent in a market that has already seen a decent price rise. Any further exacerbations of the supply/demand balance can trigger one of these events. If one does happen in silver, trust me on this one, you will not have to ask the question: "Gee I wonder if we are seeing a Commercial Signal Failure in Silver". You will know it.

Let me begin this explanation by saying that these events are relatively rare. Over the course of my career I can probably count the number of times that I have seen them occur on both hands. That is not to say that there have not been more, but in the particular markets that I actively trade, they are infrequent. However, when they do occur, the resultant price moves are spectacular; i.e. if you happen to be on the correct side. If you are not - well - you are probably no longer reading posts or having anything else to do with commodity futures markets and are gainfully employed elsewhere having had your net worth reduced by multiples.

Let's also take a Commercial Signal Failure (hereafter referred to as CSF) in a bull market. I have seen one occur in the hog market twice in my career and those were strong bear moves that resulted from chicken import bans and H1N1 outbreaks but for the most part, these things happen in a bull market.

Here is the scenario - a market begins a trending move higher. Speculators are on the long side driving the price upward with the Commercials (producers, processors, etc.) instituting hedges for risk management and selling into the speculator buying. This is all healthy and normal for the Commercials are using the futures markets for the reason that they came into being - they are locking in profit margins and eliminating price risk by transferring that risk to a speculator who is willing to assume the risk in the hopes of making money as prices move higher. It is also the reason that all bull markets that have any lasting power will always see a rise in open interest as price moves higher. Commercials are employing scale up selling programs to lock in successively higher sales prices for their production. This can be abused as it has been in gold and silver but that is another story that we all know too well.

As the price continues to move higher, commercials will attempt to take advantage of the speculative buying and will sell more and more of their expected future production. In other words, the size of their short position continues to grow as they cover their risk management needs. Now in order to maintain this short position, they are required like anyone else who has a position in the futures market to post margin. Bona fide hedgers have a distinct advantage in this however since the margin requirements for a hedger are less than that required by a speculator to post. In other words, they can control more contracts for the same amount of money than can a speculator.

The reason for this is because supposedly there is less risk for a hedger from a financial standpoint because they actually produce the commodity that they are hedging. If they lose money on the hedge, the short position, that is offset by the corresponding rise in the physical commodity. This conceivably puts them on a sounder financial footing than a speculator who is putting risk money up without having access to the underlying physical.

So far the scenario is developing like it does in every single bull market - the price rises, the speculators are on the long side, the commercials are on the short side, and the total open interest (number of contracts open) is rising. Obviously the speculators are now showing good open or paper profits on their long positions with the commercials showing paper losses on their open short positions. As price continues to rise, these commercials will also be required to post additional margin money to bring their positions back to what is called the maintenance level. The higher the price rises, the more money they must expend to meet all the clearinghouse requirements. That however is generally not a problem since these things are accounted for in their risk management programs and they have access to lines of credit which will allow them to make good on these financial requirements.

A problem develops for them however when there is an event, an occurence or development of some sort which drastically changes the supply/demand picture overnight. For example, a hard freeze could crush the Florida orange crop; a severe drought or flood could wipe out a substantial portion of a major agricultural crop, a livestock disease could surface in a major producing nation, a blight could strike the cocoa producing areas of West Africa, it could nearly anything. Whatever the event, it triggers an immediate shift in that fundamental supply and demand equation that results in a huge imbalance between demand and supply in favor of the speculators. In other words, supply has been severely impacted and sharply reduced or demand has shot up suddenly and is now grossly overwhelming supply. The result - prices spike rapidly upward and begin to accelerate higher as the market must now come to terms with the new and greatly alterated supply/demand equilibrium.

Commercials, who now find themselves on the short side of the market with a substantial position are suddenly caught flatfooted as panic buying grips the market and all offers to sell instantly disappear. The result is a massive air pocket above the market with a huge imbalance of buyers and sellers. Simply put - there are no sellers, anywhere. Everyone wants to buy and they have no one to buy from. What happens? Price must rise higher and higher until it reaches a level where the sellers, those who actually have the product, feel comfortable letting some of their supply go.

Some might say, well, what is the big deal for those commercials? After all, they have the product and while they are losing money on their short hedges, they are making it back on the physical side of thing because they actually produce the commodity. That is true and in a normal bull market, that is exactly what happens, but in a situation as above, where the event has come out of nowhere and was not anticipated and is of such magnitude that it severely throws the balance between supply/demand grossly out of balance, even these commercials are impacted.

Why is this? The answer goes back to the margin requirements. In a rising market, commercial hedgers with short positions are constantly losing money on those hedges and are required to post additional sums of money to keep current and maintain those short positions. As stated previously, to do this they draw from their own reserves which are set aside for risk management purposes. In addition they have lines of credit from various lenders who loan them the money for such purposes. But when an event alters the market dynamics to such an extent that price begins to gap higher and accelerates upward, their lines of credit are no longer sufficient to cover the paper losses on their open short positions.

In other words, they run into the exact same position as a speculator who has a market moving against him and no longer has the financial resources to maintain his margin deposit at the proper level. They are forced to get out of their positions because they have run out of money to maintain them. Unable to get any further credit and having drawn down their own reserves, they are now defenseless and must buy back the existing shorts to prevent the financial ruin of their firm.

They too now enter the buying frenzy only this time, their ability to get out of their shorts determines whether or not their firm will survive. They will hit every single available offer to sell that might appear because their very life depends on getting out. They do not care what the cost is - they must get out.

The implications are obvious - price will rise and rise and rise until every last one of those losing short positions have been cleaned out to the level that enables that firm to survive. As to how high that market will then go, it is anyone's guess. Quite frankly no one knows. It will stop at some point but by then the damage to the shorts is staggering.

Over the years I have seen entire firms go down when an event such as this transpired.

Here are a few charts detailing the results of a CSF. The first is in Live Cattle and the second is in Minneapolis Wheat.

With Live Cattle, the "black swan" event was the discovery of a cow in Canada back in 2003 that came down with "mad cow" disease resulting in the US authorities closing the border to all shipments of Canadian beef and live cattle. The result was an immediate shift in the supply/demand balance with US supply sharply curtailed and unable to meet the then existing demand. Price shot sharply higher moving limit up 8 days in a row, 5 of those days being gaps in which the market basically shut down because there was no one to sell.

I can still remember the cries and pleas from the commercials who were members of the CME for the exchange to do something because they could not get out and were being ruined.

The Minneapolis Wheat market, back in the winter of 2008, was roiled by a perfect storm of developments that seemed to come together all at once. Horrific crop weather, soaring demand, export bans from wheat growing countries, it just all hit at once. The result was the most spectacular Commercial Signal Failure that I have ever seen. Price soared from an already expensive $10.00/bushel to nearly $24.50 for a single bushel of this wheat! The market literally did not trade for days on end as it opened at limit bid day after day with absolutely no one to sell. There were more than a few firms who were destroyed as a result of their short hedges in this market.

I do want to point out something about these CSF's. Note that once they run their course, the market generally collapses and gives back a very large percentage of its overall gains. That is because once all the Commercials have finished buying back their bleeding short positions, there is no one left to buy and prices now come tumbling back to earth. In some cases, all the price rise is erased; in other cases a substantial portion are given back but the market then finds a footing at a new and higher price level.

As with any market, the potential always exists for such a development especially when there exists a very large short contingent in a market that has already seen a decent price rise. Any further exacerbations of the supply/demand balance can trigger one of these events. If one does happen in silver, trust me on this one, you will not have to ask the question: "Gee I wonder if we are seeing a Commercial Signal Failure in Silver". You will know it.

Subscribe to:

Posts (Atom)