"When misguided public opinion honors what is despicable and despises what is honorable, punishes virtue and rewards vice, encourages what is harmful and discourages what is useful, applauds falsehood and smothers truth under indifference or insult, a nation turns its back on progress and can be restored only by the terrible lessons of catastrophe." … Frederic Bastiat

Evil talks about tolerance only when it’s weak. When it gains the upper hand, its vanity always requires the destruction of the good and the innocent, because the example of good and innocent lives is an ongoing witness against it. So it always has been. So it always will be. And America has no special immunity to becoming an enemy of its own founding beliefs about human freedom, human dignity, the limited power of the state, and the sovereignty of God. – Archbishop Chaput

Trader Dan's Work is NOW AVAILABLE AT WWW.TRADERDAN.NET

Ever since that last USDA report, wherein the agency surprised the market with a big jump in planted acreage, the beans have been on the defensive. That report, plus the continuation of very good growing conditions changed the dynamic completely in the beans. Prior to the report, the focus of many traders was the continued tightness in old crop carryover. Simply put, the market was of a mind to ration demand so as not to run out of available bean supply prior to this year's harvest.

It was that old crop carryover tightness that had been the driving factor particularly in the July and to some extent, the August bean contracts. New crop November had been yanked, tugged, pulled and generally distorted by the buying in those former mentioned contracts.

Now that the Quarterly report is out of the way, traders are looking forward to a massive harvest based on USDA weekly conditions ratings, as well as field reports. The result has been a complete and rapid sentiment shift that has caught many of the hedge funds leaning on the long side of this market. They are getting out of Dodge very rapidly based on what we are seeing in the weekly Commitment of Traders reports. However, as of last Tuesday, they were still net long. I am sure that has changed by now as the market has lost some 82 points since then.

I expect to see this week's COT reports showing them to having moved over to the short side of the market.

The market is now anticipating this coming Friday's Supply and Demand report. Based on what we get out of that, we could see even more weakness if end users feel that they can buy, "Hand to Mouth" to meet their needs as they wait for harvest to begin. While the beans are certainly not out of the woods, as they are essentially more dependent on August weather compared to corn, it is not inconceivable that we could see them near the $12.00 level without some sort of bullish surprise in this report ( or a shift to a hot, dry weather pattern across the corn belt).

Indicators on the weekly chart are pointing lower. A breach of the $12.00 support zone would suggest an initial move to $11.50 and then to $11.00- $10.80 should that fail.

On the upside, this week's gap lower is initial resistance starting near $12.86 and extends to $13.00.

A quick note on gold - it is firm due to geopolitical events - first it was Ukraine, then it was Iraq, and now it is Israel and Hamas. One wonders, with the various commodity indices all retreating lower once again, how long the geopolitical concerns can keep it supported. Gold needs support from rising commodity prices.

Not that it has made the least bit of difference to the continuing price rise over the last year, but each new weekly high in this very risk sensitive index, has come with a lower reading in the RSI. Note that I have smoothed the indicator a bit to weed out a bit of the "roughness". That being said, the RSI reading has not once in the last year, surpassed its high reading made in March 2013 and again in August 2013. Upside momentum is waning but it does not yet seem to matter. The index has relentlessly powered higher.

I do not believe one can call a definitive top in this market until, at the very least, the support level near 1080 might give way on a weekly closing basis. One should however note these negative or bearish divergences and at least exercise some caution.

Traders who are long with large open profits might want to get a bit of downside protection in the form of puts or covered calls on a portion of their positions just in case this index were to finally confirm any of these divergences.

The problem for the bears has been the ultra low interest rate environment. It has essentially made stocks the only game in town as far as obtaining a decent rate of return on invested money. Until that changes, bulls will more than likely continue with their heretofore successful practice of buying dips. Eventually the music will stop but timing that over the last year has been a fool's errand. All a trader/investor can do is to go with the money flow until something changes technically to indicate that the party is over. For now, in spite of the divergence warnings, the good times continue to roll for the bulls.

Benevolent weather and falling demand ( in anticipation of weaker prices ahead ) has led to heavy selling across the entirety of the grain floor this morning. The result is that my grain index has notched a 42 month low! This is very welcome news for the livestock and poultry industry as well as for consumers who can expect to see lower food prices ahead ( assuming of course that the trade will eventually pass through the savings).

I should also note here, that according to the most recent Commitment of Traders data through 7-1-2014, Managed Money or Hedge Funds still remain as net longs in the corn market in spite of the fact that corn futures scored a 4 year low today. Also this same category remain net long in soybeans as well even though they have been caught on the wrong side of the market and are now in the process of liquidating long positions at a very rapid clip ( not to mention starting to build shorts).

This informs us that if this category decides to get aggressively short, we have further downside to go across the corn and bean markets.

Crude oil prices are also continuing to weaken although they remain high but are at least headed in the direction that will benefit consumers and business for the moment.

The weakness in crude oil and its products today, especially gasoline, is weighing on the Goldman Sachs Commodity Index, which I wish to remind the reader is excessively weighted ( in my opinion ) in its energy component.

Notice the sharp retreat from the top resistance zone which has knocked the index back to a 3+week low. Also note that it has fallen back below the recent breakout point near 660.

I am also noticing that Cotton prices are trading near an 19 month low today. That will help keep the cost of clothing from rising too abruptly... more good news for the cash strapped consumer. Cotton fiber competes with the synthetics most, if not all of, which are tied to crude oil prices.

W

ith the yield on the Ten Year Treasury dropping to 2.616% today, it would appear that inflation worries, at least in the area of commodity prices in general, have subsided for the immediate moment.

The ADP numbers yesterday were indeed a precursor to today's very strong payrolls number. The market was expecting a good number and that is exactly what it got - and more. Going into the report a 215K increase was the consensus - instead we got a 288K reading.

A bit later this AM, the June ISM service sector numbers came out and that also helped to confirm that strong jobs number. The employment component of that series came in at 54.4 against a 52.4 reading in May.

Stocks loved the number as the Dow rose above 17000. The S&P 500 and the Russell 2000 both moved higher as well. Any time weakness appears and it looks as if the Bears are finally going to get their day in the sun, back up these equity markets go only to set another new all time high. It is nothing short of astonishing. Fighting the tape has been a fool's errand when it comes to these equity markets.

The VIX, or Volatility Index ( I prefer to call it the Complacency Index ) is flirting with levels last seen in February 2007! Amazing!

The yield on the Ten Year rose as high as 2.69%. According to one of the CME markets, the odds of a rate hike by the Fed at its June 2015 FOMC meeting rose to 57%. Yesterday the odds were 51%. Last month the odds were 43%. It is clear that the a majority are coming around to the view that higher rates are in store next year. If the market becomes convinced that the Fed is going to be able to stay on top of any nascent inflationary pressures, gold is going to lose some of its current friends.

I suspect that today's strong number is going to shift more of the focus on the wages numbers coming our way in the future. Traders/investors are going to want to see some evidence of wage inflation. So far they do not seem concerned. As long as that is the case, the Fed can remain accommodative and will not be in a hurry to kick rates higher. Still, one can clearly see a subtle shift coming in regards to sentiment towards higher rates.

As far as gold is concerned, the metal looks as if geopolitical events in Iraq are continuing to provide some support. The stronger Dollar coming on the heels of the payrolls number, provided pressure. The lack of wage inflation did likewise. However, while the market bent, it did not break. The geopolitical premium remains. Also, while I have noticed that the TIPS spread has weakened somewhat this week, it is still up near 6 month highs.

If grain prices continue to work lower, it will be up to the energy complex to bring support to the commodity sector as far as inflationary aspects are concerned. Right now crude is continuing to weaken and has fallen down near that support zone I noted on the crude chart I put up in yesterday's post.

Coffee, sugar, cotton, soybeans, wheat and corn are all lower today - along with crude, heating oil and unleaded gasoline. Cattle are strongly higher as news hit the market after the close of pit session trading yesterday of a record $1.58 paid for cattle in the Southern Plains. I had to double check that price print as I thought I was hallucinating. WOW! those who have cattle to sell are sitting very pretty right now. By the way, as a side note, I just picked up my brisket for my July 4th barbeque - GREAT GOOGLY MOOGLY! I wonder how it now compares to caviar as far as price per ounce? AS I have said before in many posts - there is not going to be much if any relief in sight for meat prices for the remainder of this summer. We are going to have to wait for the 4th quarter, but especially for Q1 2015 for any significant relief.

On the currency front - ECB President Draghi was out making some dovish comments once again. Those, while not the main mover in the Forex arena, certainly did nothing to soothe any Euro bulls. One gets the distinct impression, especially after today's payrolls number, that interest rates, if they are going to go up, will certainly be doing that here in the US, well before they will be over in the Eurozone. That should keep the Dollar supported at the expense of the Euro.

You can see on the chart of the long bond that prices have been falling recently and have broken the uptrend line shown. Bonds have bounced however from the support zone noted. They will need to at a bare minimum, take out that level before we can say with any degree of certainty that a serious downtrend has begun. It is too early for that right now. We will need more confirmation in the price action.

If however we begin to see a STEADY series of good payrolls numbers, along with rising wages, I fully expect this chart to break down for good. The jury is out so we wait.

Happy Independence Day ( July 4th) to my American readers ( and to anyone else who might be celebrating along with us). When I look at the incredible system of government given to us by our Founding Fathers, and then shift my attention to what we now have left of it, I fear my kids and grandkids are not going to be able to see anything remotely in common with it by the time they are grown. Liberty is precious precisely because it is so rare among the annals of human history. This generation seems to have forgotten that although one wonders if they ever knew it in the first place.

I will get some updated charts up later... busy morning...

Once again we got another surprise in the crude stocks number as it hit the wires this morning. The trade was looking for a drop of 1.7 million barrels. Instead it got 3.2 million drop.

Crude oil had been weaker ahead of the data on concerns that Libyan oil exports might be on the rise but it rebounded when the EIA data hit.

Ominously, the market could not hold its gains and begin to retreat once again.

This price action is confirming my suspicions that the massive hedge fund net long position in the market ( a position that was drawn down somewhat in last week's COT data) is becoming more of a concern to players. When rallies are attracting long liquidation instead of a batch of brand new hot money flows, one has to be cautious.

Here is the chart.

As I noted yesterday, the market could fall down to the uptrend line and still maintain the bullish posture. That comes in near $103.50. It is also the 25% Fibonacci Retracement Level of the entire rally that began early this year. See the red ellipse....

The former resistance level, now turned support, near the $105 level, finally gave way today. Under normal circumstances, the loss of that level would portend lower prices. However, we have a big payrolls number out tomorrow and there is the possibility that if the number comes out stronger than what the market currently expects ( and it does look as if the market is expecting a good one - certainly copper does ) then we might see crude move higher on ideas that consumers are more likely to maintain strong demand domestically for gasoline as they head out for summer vacations. That plus the fact that economic activity might increase.

I have no idea what we might get on that volatile payrolls number but am just postulating a possible market reaction.

The flip side is that if the number is poor, crude could succumb to further downside follow through. We will just have to wait and see.

I will try to get some additional commentary up later today. It has been a very busy day....

A quick note - gold continues to struggle with this $1330 level. There has been a fairly rapid build in speculative longs in that market as well so the longer it cannot break through this current cap, the more the odds increase of some stale long liquidation. Again, it will be at the mercy of the payrolls data tomorrow.

It will be interesting to see if we do get a strong number, how gold reacts to it. Many will expect a strong number to pressure the price of the metal as it will lend credence of a sooner-than-expected tightening of interest rates by the Fed. It is possible however that some might see a strong number as a key ingredient to the inflation recipe. Again, I have no way of knowing how this market will respond.

Guess what - no one else does either, in spite of their reckless assertions to the contrary.

"Modest" seems to be the key word to describe global manufacturing growth at the moment. Overnight data out of China and Europe, and then this morning in the US, shows readings above the 50 level ( over 50 is expansion; under 50 is contraction) but nothing spectacular. Equities in particular seem to welcome that news as it is a perfect environment for the bulls - growth, but not fast enough to kick up serious inflation worries. As I type these comments, the S&P 500 just scored another all-time high and the Russell 2000 is once again knocking on the door of its best print ( so much for this index showing signs of fatigue - see that previous post of mine last week).

Copper is not quite sure what to do with the numbers. While copper bulls are glad to see the stronger data, copper bears are of the view that the growth is not fast enough to sustain significantly higher prices for the metal. It did manage a breakout above that resistance zone on its chart and notched a nearly 4 month high today but it appears to be a bit hesitant to extend strongly higher yet. One gets the idea that while sentiment towards copper is markedly improved, that folks are wondering just how much strength in the global economy there is. It may have to wait until this Thursday when we get the payrolls numbers before it makes a bigger move.

For now, while traders may not feel confident enough about it to chase it higher, they look to be ready to buy dips. Chinese double counting and triple counting fears seem to be well in the rear view mirror at this point.

It is interesting to note the action in crude oil in today's session. Brent crude liked the manufacturing data, especially from China, and WTI did as well, but it has faded nearly $1.00/bbl as I am typing these comments up. As I was going over the last COT reports for crude this past Friday, I noticed that the massive, net long position of the hedge funds had been whittled back somewhat. While sentiment towards crude among that group was still extremely bullish, they were pulling some money off of the table. I am watching this closely to see if they will come back in with fresh money at the start of this new month or if they are content to take profits on subsequent rallies higher.

For now, price has stalled up near $107.50 and has retreated to the point of the previous breakout, namely the $105 level. Support extends down from this level towards $104.50. Thus far the market is showing no signs of breaking down as support is holding but with that very large hedge fund long position in this market, any break of a chart support level will get mighty interesting, might fast. Price could fall, in the event of a bout of long liquidation, as far as $103.50 or so and do no damage to the bigger uptrend.

Crude's behavior, along with copper, should tell us a great deal about what big-monied speculative interests are thinking in regards to global and domestic growth.

Grains and beans continued moving lower today. Yesterday's crop condition reports were just icing on the cake as far as the bears were concerned. That earlier report showing the stunningly large bean acreage set the tone and it has been negative since. The corn condition actually got even better ( 75% Good/Excellent) in the conditions report yesterday afternoon.

The chart scored a near 5 month low today.

Finally! We finally got an updated number from the GLD holdings yesterday. It showed a nice influx of some 5.05 tons of gold since the last updated number. That is a nice "positive" strike three. I mean by that, you had the gold price moving higher yesterday, the mining shares moving higher and the GLD showing an increase of 5 tons. That is exactly what one wants to see if they are a gold bull. That, plus the fact that the US Dollar index fell below 80 on its chart.

Gold moved higher in spite of the fact that crude oil moved lower yesterday and the grains imploded. That is even more impressive.

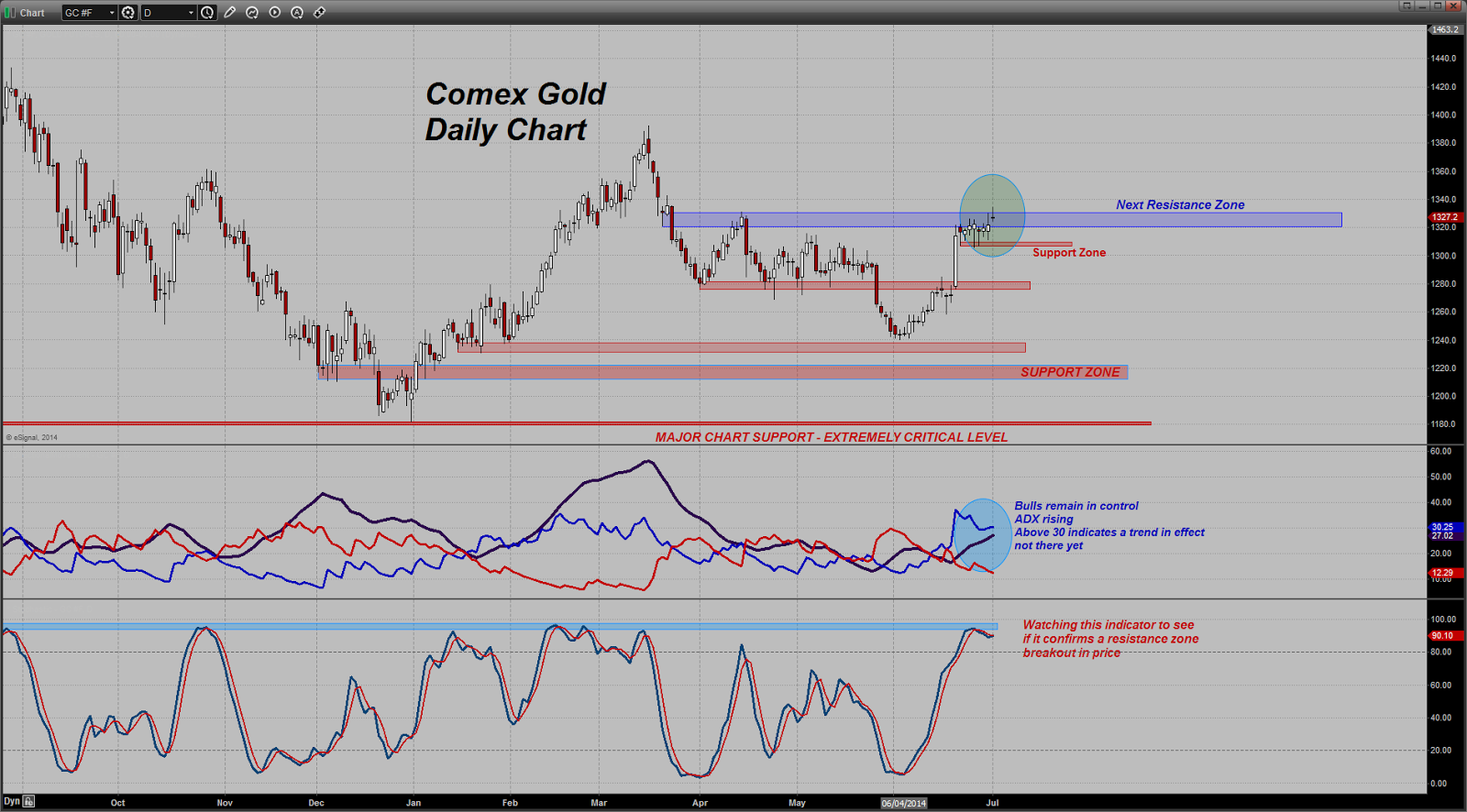

As far as today's price action goes for the yellow metal, it is attempting to break through and away from this resistance zone noted on the chart. Like copper, the market appears to be pausing here to evaluate the current price level. Bulls appear hesitant to get too aggressive while bears are trying to dig in.

If we get a clean push past the top of this zone, the next target is up near the $1360 level. If that were to give way, $1390 comes into play.

I am closely watching the ADX and some other indicators to see whether this market is going to reverse here or will extend. Ranging indicators are near overbought levels commensurate with moves lower in price. However, and this is important, bulls need to push price up to get us to move away from the range trade indicators to the trending indicators. They have not done that yet ( they are close however).

Price could fall back towards $1305 - $1306 and still be okay but bulls would not want to see that fail or it would portend a deeper retracement lower, especially if the market were to lose psychological support at $1300.

For now we wait. Longs - stay sharp here and be alert. One wonders if yesterday's big buyers will return right away or will wait for a dip lower.

Today's USDA reports really did a number on this index that I have created for my own analysis purposes. The unexpected data showed supply outrunning current expected levels of demand and forced the market to adjust to the new set of fundamentals.

If you note the index, it is at a 5 month low!

A couple of things to note here that I was unable to get to this morning amidst the hustle and bustle of trading activity. First, corn demand has fallen off because feed demand is falling off. The reason is because we now know that there are less piggy mouths around to feed than previously expected. Also, cattle numbers are well off last year's levels as well. Less animals to feed means less corn demand.

Secondly, even though planted acreage estimates for corn are lower than last year, traders are expected the harvested crop to actually come in larger than last year. The reason is because we have thus far had nearly ideal growing conditions. The crop looks terrific at this point as it enters the key pollination stage and for now, forecasts look benign.

Wheat prices are low but global supplies are ample and US prices have had to respond to increased competition from other nation suppliers.

I do want to add another note here - today is both the end of the month and the end of the quarter. End of the month positioning is bad enough but throw in a good dose of end of the quarter book squaring, and all manner of strange price moves can be seen.

One look at the chart says it all - Copper is knocking on the door of overhead chart resistance and is threatening an upside breakout.

The catalyst has been continued improvement in recent Chinese manufacturing economic data. Traders are also optimistic that this evening's upcoming overnight release of China's monthly purchasing managers' index is going to be positive.

Also, today's US pending home sales data was a big mover of the market. Sales rose 6.1% in May compared to the previous month. The estimates were for a very modest 1.1% increase. The red metal leapt higher when the data hit the wires as it was much better than expected. Bears were caught off guard by the surprisingly strong number and wasted no time covering.

Copper bulls are banking on improved numbers coming from the two largest consumers of the red metal ( China and the US).

Also, there is behind the scenes talks occurring among banks and traders caught up in the double and triple counting metal schemes to split losses. That seems to have lessened the impact from any expected forced sales of copper in the event that the Chinese authorities force the loans to be called.

It's funny isn't it how one day the market is terrified of losses and then the next day it could care less. Such are the fleeting vagaries of sentiment. One never knows when it will change or what it will decide to focus on from day to day. Let's just say that for now, looking at the chart, Copper is convinced that economic data is going to be improving as we move forward into the summer months.

Let's keep a very close eye on this chart. It is one of the most accurate indicators of global economic activity that I know of.