Friday, February 25, 2011

4 Hour Gold Chart - End of trading week

I will have some daily and weekly charts up of both the metals this weekend along with some other markets that impact them both.

Backwardation Structure appears to Easing in Silver - but is it?

Reposting from earlier this AM:

The strong backwardation structure that has existed in the silver market for some time, at least on the futures board, appears to be easing even as the March contract goes into its delivery period. This is happening even as we continue getting reliable reports of tightness in the spot market and long waiting periods for silver bars.

March silver's open interest is drawing down rapidly having dropped a bit over 14,000 contracts in yesterday's wild session. There is a decent amount of rolling out of March into May based on the exchange's today, but it is not a one for one roll. Both longs and shorts bailed out yesterday.

There are still a considerable number of contracts open in March, 14,259 to be exact, but we have today's session yet which no doubt will see a further reduction in that contract month.

If a squeeze is going to occur, we will need to see the March return to a premium to the May and preferably also to the July.

Here are the spread charts detailing the change from one of backwardation to a more normal contango situation. When a backwardation structure exists, the spread line will be above zero; when contango exists, the spread will be below zero.

As you can see, the backwardation structure has been easing. At the risk of repeating, if there will be a move to push the shorts during the delivery period in the March next week, this spread line will indicate it by moving back above zero against the May and if it is particularly strong, also against the July contract. I do wish to point out however that while the backwardation structure of the March has eased it is just barely in contango.

Keep in mind that this chart is a snapshot in time and can change so we will need to continue to monitor this for further developments.

To get an even more accurate read on this we would need to capture a snapshot in time comparing the spot silver market bid/offer to the current bid/offer of the nearby March silver contract. At the time I am posting this, spot silver is actually trading about 6 - 7 cents higher than the nearby March futures contract which makes the current structure of the Comex silver market seemingly at odds with the physical market once again. In other words, we have a rather strong backwardation in the physical market but an easing backwardation moving towards contango on the paper market.

An ideal situation for a short squeeze exists when both the futures board and the spot market are speaking with the same voice. In the case of what we have now, if the physical market is as tight as it seems to be, there should be a large number of players standing for delivery in the March. AFter all, if you are a large buyer of silver, and you can get the exact thing by buying a March futures contract at what is a DISCOUNT to the physical market, who in their right mind would not want to do that? If nothing else, a player with the right connections could arbitrage the setup and guarantee an immediate and healthy profit.

Stay tuned on this one. With Silver there is never a dull moment.

The strong backwardation structure that has existed in the silver market for some time, at least on the futures board, appears to be easing even as the March contract goes into its delivery period. This is happening even as we continue getting reliable reports of tightness in the spot market and long waiting periods for silver bars.

March silver's open interest is drawing down rapidly having dropped a bit over 14,000 contracts in yesterday's wild session. There is a decent amount of rolling out of March into May based on the exchange's today, but it is not a one for one roll. Both longs and shorts bailed out yesterday.

There are still a considerable number of contracts open in March, 14,259 to be exact, but we have today's session yet which no doubt will see a further reduction in that contract month.

If a squeeze is going to occur, we will need to see the March return to a premium to the May and preferably also to the July.

Here are the spread charts detailing the change from one of backwardation to a more normal contango situation. When a backwardation structure exists, the spread line will be above zero; when contango exists, the spread will be below zero.

As you can see, the backwardation structure has been easing. At the risk of repeating, if there will be a move to push the shorts during the delivery period in the March next week, this spread line will indicate it by moving back above zero against the May and if it is particularly strong, also against the July contract. I do wish to point out however that while the backwardation structure of the March has eased it is just barely in contango.

Keep in mind that this chart is a snapshot in time and can change so we will need to continue to monitor this for further developments.

To get an even more accurate read on this we would need to capture a snapshot in time comparing the spot silver market bid/offer to the current bid/offer of the nearby March silver contract. At the time I am posting this, spot silver is actually trading about 6 - 7 cents higher than the nearby March futures contract which makes the current structure of the Comex silver market seemingly at odds with the physical market once again. In other words, we have a rather strong backwardation in the physical market but an easing backwardation moving towards contango on the paper market.

An ideal situation for a short squeeze exists when both the futures board and the spot market are speaking with the same voice. In the case of what we have now, if the physical market is as tight as it seems to be, there should be a large number of players standing for delivery in the March. AFter all, if you are a large buyer of silver, and you can get the exact thing by buying a March futures contract at what is a DISCOUNT to the physical market, who in their right mind would not want to do that? If nothing else, a player with the right connections could arbitrage the setup and guarantee an immediate and healthy profit.

Stay tuned on this one. With Silver there is never a dull moment.

India moves towards direct Yuan convertibility

Thanks again to David for providing what I view as a very significant news article out of the Times of India.

You might recall that I had posted an article dealing with the concentrated efforts by the Chinese authorities to work towards this very thing just recently- namely, the effort to make the Yuan an international currency. The biggest hindrance to this has been this lack of convertibility. Once this issue is resolved, and it looks as if there is now a serious, concerted effort in this direction that is gaining in popularity, it is going to be yet another nail in the coffin of the US Dollar.

You might recall that I had posted an article dealing with the concentrated efforts by the Chinese authorities to work towards this very thing just recently- namely, the effort to make the Yuan an international currency. The biggest hindrance to this has been this lack of convertibility. Once this issue is resolved, and it looks as if there is now a serious, concerted effort in this direction that is gaining in popularity, it is going to be yet another nail in the coffin of the US Dollar.

One Wise Central Bank

The following headline from a Dow Jones Newswire Service report says it all. You can be assured that many other Central Banks are also seeing the yellow metal in a favorable light.

Note the relatively low levels of gold in the reserves of Brazil, a rising economic powerhouse and an increasingly important buyer of US Treasuries. Look for this nation to begin an acquistion process of gold in the months and years ahead.

DJ Argentina's Gold Bet Pays Off As Metal Nears New Highs

By Ken Parks

Of DOW JONES NEWSWIRES

BUENOS AIRES (Dow Jones)--The Central Bank of Argentina's decision to add

gold to its foreign reserves nearly seven years ago has paid off, with the

precious metal trading close to the record highs observed in late 2010.

The central bank reported 9.41 billion pesos ($2.33 billion) of gold on its

balance sheet at the end January, equivalent to nearly 4.5% of its total

foreign-currency reserves of ARS210.51 billion, according to data published on

its website. A year earlier, those holdings were valued at ARS7.28 billion.

Argentina's central bank significantly increased its holdings of gold during

the first seven months of 2004, when it purchased 1.76 million troy ounces for

an average price of $398.87 per ounce.

According to the institution's most recent annual report to Congress, the

central bank held 1.76 million ounces of gold at the end of 2009.

Alfonso Prat-Gay, who was president of the central bank from December 2002

until September 2004, said that at that time bank staffers opposed the purchase

of gold because they feared the political and legal repercussions had the

country's creditors been able to embargo the transaction. Argentina defaulted

on about $100 billion in sovereign debt in 2001.

"The bank had gotten rid of all of its gold in the 1990s and at that moment

it didn't have any exposure to gold. It seemed to us a prudent policy to have

5% of our liquid reserves in gold and at the time we were prepared to increase

that position in the future," he said in an emailed statement to Dow Jones

Newswires.

Citigroup Inc (C) expects gold to rise 7.8% this year to $1,445 an ounce

after averaging $1,340 last year. If correct, that could make gold one of the

highest-yielding assets in the Central Bank of Argentina's foreign-reserve

holdings this year, with benchmark interest rates in the U.S. and Europe still

at rock bottom lows.

Gold is viewed by some investors as a hedge against inflation and volatile

currencies. Earlier this month, gold inched closer to becoming a currency after

U.S. banking giant J.P. Morgan Chase & Co. (JPM) said it would allow clients to

use the precious metal as collateral in some transactions in which banks

typically accept only U.S. Treasury bonds and stocks.

Barrick Gold Corp. (ABX, ABX.T), the world's largest producer of the precious

metal, said in an interview published Feb. 1 in the Wall Street Journal that it

expects central banks to move more of their monetary reserves into gold this

year due to concerns about the value of their U.S. dollar holdings amid a

sluggish U.S. economy and rising government debt.

"Nothing in this world is safer than physical gold and its opportunity cost

has never been as low as it is today given risk-free interest rates are at

zero. All central banks should have an important exposure to gold. In my

opinion 20% of reserves should be a floor," said Prat-Gay, who today is a

congressman and a member of the Coalicion Civica party.

A central bank spokesman contacted by Dow Jones Newswires said the monetary

authority doesn't comment about its reserve policy.

Although gold represents only a small percentage of its reserves, the Central

Bank of Argentina's holdings are among the largest of its peers in Latin

America.

The Central Bank of Peru held 1.1 million troy ounces, valued at $1.48

billion, at the end of January, or about 3.3% of its reserves. Brazil's central

bank owned 1.08 million troy ounces of gold worth about $1.43 billion,

equivalent to just 0.5% of its total reserve assets.

Chile's central bank had less than 0.05% of its reserves in gold with

CLP5.121 billion ($10.7 million) on its balance sheet at the end of January.

Meanwhile, the Bank of Mexico held about 230,000 troy ounces at the end of

December, with the value of its holdings of physical gold and gold swaps

totaling $322 million, a drop in the bucket compared to its foreign reserves of

$120.59 billion.

-By Ken Parks, Dow Jones Newswires; 54-11-4103-6740, ken.parks@dowjones.com

(END) Dow Jones Newswires

02-25-11 1410ET

Copyright (c) 2011 Dow Jones & Company, Inc.

Note the relatively low levels of gold in the reserves of Brazil, a rising economic powerhouse and an increasingly important buyer of US Treasuries. Look for this nation to begin an acquistion process of gold in the months and years ahead.

DJ Argentina's Gold Bet Pays Off As Metal Nears New Highs

By Ken Parks

Of DOW JONES NEWSWIRES

BUENOS AIRES (Dow Jones)--The Central Bank of Argentina's decision to add

gold to its foreign reserves nearly seven years ago has paid off, with the

precious metal trading close to the record highs observed in late 2010.

The central bank reported 9.41 billion pesos ($2.33 billion) of gold on its

balance sheet at the end January, equivalent to nearly 4.5% of its total

foreign-currency reserves of ARS210.51 billion, according to data published on

its website. A year earlier, those holdings were valued at ARS7.28 billion.

Argentina's central bank significantly increased its holdings of gold during

the first seven months of 2004, when it purchased 1.76 million troy ounces for

an average price of $398.87 per ounce.

According to the institution's most recent annual report to Congress, the

central bank held 1.76 million ounces of gold at the end of 2009.

Alfonso Prat-Gay, who was president of the central bank from December 2002

until September 2004, said that at that time bank staffers opposed the purchase

of gold because they feared the political and legal repercussions had the

country's creditors been able to embargo the transaction. Argentina defaulted

on about $100 billion in sovereign debt in 2001.

"The bank had gotten rid of all of its gold in the 1990s and at that moment

it didn't have any exposure to gold. It seemed to us a prudent policy to have

5% of our liquid reserves in gold and at the time we were prepared to increase

that position in the future," he said in an emailed statement to Dow Jones

Newswires.

Citigroup Inc (C) expects gold to rise 7.8% this year to $1,445 an ounce

after averaging $1,340 last year. If correct, that could make gold one of the

highest-yielding assets in the Central Bank of Argentina's foreign-reserve

holdings this year, with benchmark interest rates in the U.S. and Europe still

at rock bottom lows.

Gold is viewed by some investors as a hedge against inflation and volatile

currencies. Earlier this month, gold inched closer to becoming a currency after

U.S. banking giant J.P. Morgan Chase & Co. (JPM) said it would allow clients to

use the precious metal as collateral in some transactions in which banks

typically accept only U.S. Treasury bonds and stocks.

Barrick Gold Corp. (ABX, ABX.T), the world's largest producer of the precious

metal, said in an interview published Feb. 1 in the Wall Street Journal that it

expects central banks to move more of their monetary reserves into gold this

year due to concerns about the value of their U.S. dollar holdings amid a

sluggish U.S. economy and rising government debt.

"Nothing in this world is safer than physical gold and its opportunity cost

has never been as low as it is today given risk-free interest rates are at

zero. All central banks should have an important exposure to gold. In my

opinion 20% of reserves should be a floor," said Prat-Gay, who today is a

congressman and a member of the Coalicion Civica party.

A central bank spokesman contacted by Dow Jones Newswires said the monetary

authority doesn't comment about its reserve policy.

Although gold represents only a small percentage of its reserves, the Central

Bank of Argentina's holdings are among the largest of its peers in Latin

America.

The Central Bank of Peru held 1.1 million troy ounces, valued at $1.48

billion, at the end of January, or about 3.3% of its reserves. Brazil's central

bank owned 1.08 million troy ounces of gold worth about $1.43 billion,

equivalent to just 0.5% of its total reserve assets.

Chile's central bank had less than 0.05% of its reserves in gold with

CLP5.121 billion ($10.7 million) on its balance sheet at the end of January.

Meanwhile, the Bank of Mexico held about 230,000 troy ounces at the end of

December, with the value of its holdings of physical gold and gold swaps

totaling $322 million, a drop in the bucket compared to its foreign reserves of

$120.59 billion.

-By Ken Parks, Dow Jones Newswires; 54-11-4103-6740, ken.parks@dowjones.com

(END) Dow Jones Newswires

02-25-11 1410ET

Copyright (c) 2011 Dow Jones & Company, Inc.

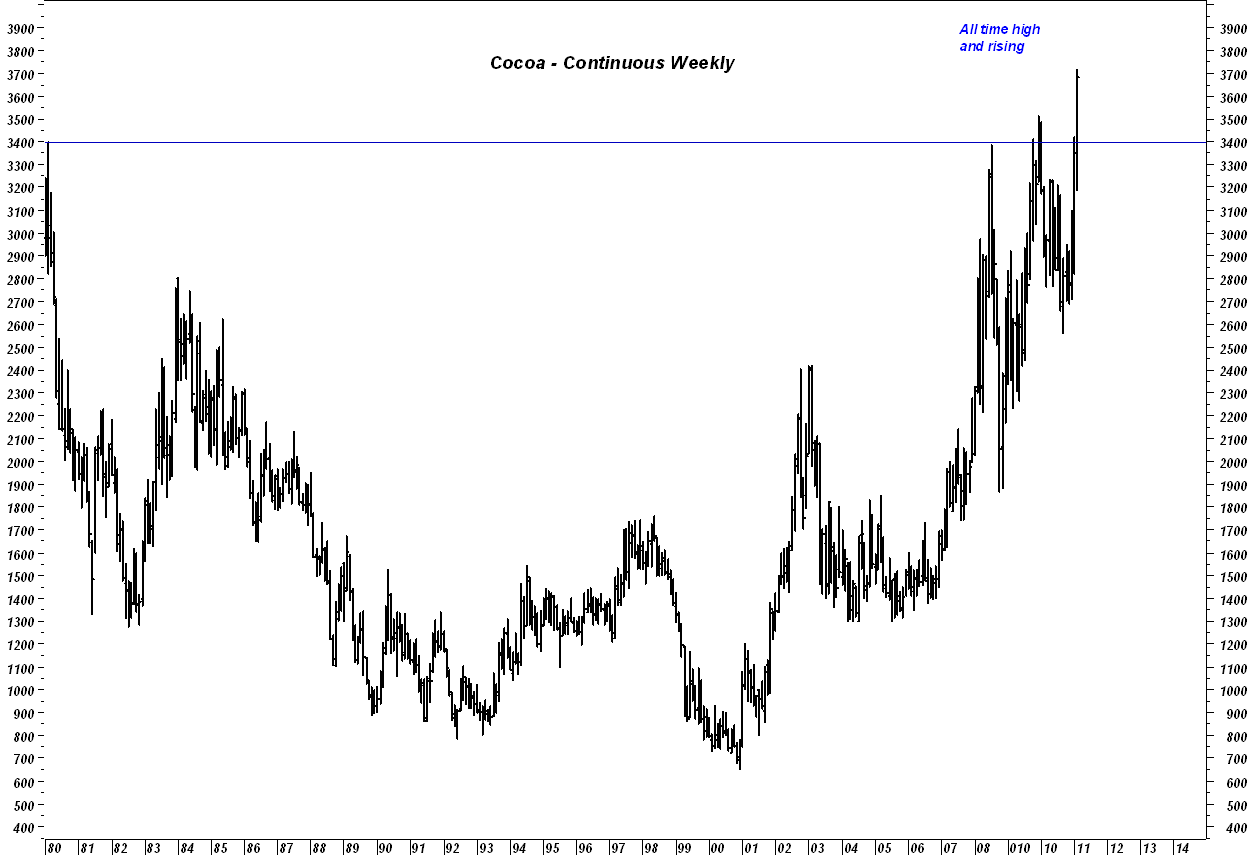

Don't mess with my Chocolate

Look, I can handle price rising for all kinds of food. I understand that the Fed has created a perfect storm in the commodity markets with its shortsightedly destructive QE policies. And while I resent the fact that they are intent on destroying the US Dollar and with it, the way of life for my kids and their grandkids, nothing riles me more than to see what they have done to my chocolate. When inflation hits this commodity, now you are getting personal. After all, a man's chocolate is sacred - I might add here that I suspect that there are a lot more women who would second this.

Just make sure that if you start hoarding chocolate, that you don't stash it in the attic!

Just make sure that if you start hoarding chocolate, that you don't stash it in the attic!

Hedgies run back into Grains - Up goes the CCI

For those of you who might have seen the original "Karate Kid" movie, you will recall that great scene where Mr. Miyagi, played by the now deceased Pat Morita in instructing his young student, Daniel LaRusso in the finer arts of waxing classic automobiles. His famous lines: "Wax On; Wax Off", come to my mind with increasing frequency these days in observing the wild price swings occuring in the commodity markets.

Take corn for example - Earlier this week the hedge funds were throwing it all away on the stupid notion that a rising crude oil price would force people to give up eating and somehow also suppress the appetite of livestock and poultry. WAX OFF

Today they are back in there loading up on the yellow foodstuff after end users bought every bit of what they threw away and reminded the world that human and animal appetites do not particulary care what the cost of crude oil might happen to be. WAX ON

Tomorrow, who knows.

The result of all this buying across the food complex has been to push the CCI, the Continuous Commodity Index right back up against its recent all time high, setting up a very real possibility that the index will CLOSE at a new all time high price. Were it not for the current bout of weakness in the precious metals, the CCI would have gone on to make an all time high once again.

Maybe the bond market will eventually get the message and come out of its fairy tale, Fed-created La La land.

Take corn for example - Earlier this week the hedge funds were throwing it all away on the stupid notion that a rising crude oil price would force people to give up eating and somehow also suppress the appetite of livestock and poultry. WAX OFF

Today they are back in there loading up on the yellow foodstuff after end users bought every bit of what they threw away and reminded the world that human and animal appetites do not particulary care what the cost of crude oil might happen to be. WAX ON

Tomorrow, who knows.

The result of all this buying across the food complex has been to push the CCI, the Continuous Commodity Index right back up against its recent all time high, setting up a very real possibility that the index will CLOSE at a new all time high price. Were it not for the current bout of weakness in the precious metals, the CCI would have gone on to make an all time high once again.

Maybe the bond market will eventually get the message and come out of its fairy tale, Fed-created La La land.

This time it's Vietnam dealing with Inflation

One nation after another across Asia is fighting this beast. Yesterday we saw it was India, previously we have seen it was China, and now we see it is Vietnam. More fuel for the gold and silver demand fire.

Thanks to Paul for sending this my way.

Headline:

http://online.wsj.com/article/SB10001424052748703842004576163483115005302.html

Thanks to Paul for sending this my way.

Headline:

Vietnam Steps Up Its Inflation Fight

You can read the entire article here:http://online.wsj.com/article/SB10001424052748703842004576163483115005302.html

Backwardation Structure appears to Easing in Silver - but is it?

The strong backwardation structure that has existed in the silver market for some time, at least on the futures board, appears to be easing even as the March contract goes into its delivery period. This is happening even as we continue getting reliable reports of tightness in the spot market and long waiting periods for silver bars.

March silver's open interest is drawing down rapidly having dropped a bit over 14,000 contracts in yesterday's wild session. There is a decent amount of rolling out of March into May based on the exchange's today, but it is not a one for one roll. Both longs and shorts bailed out yesterday.

There are still a considerable number of contracts open in March, 14,259 to be exact, but we have today's session yet which no doubt will see a further reduction in that contract month.

If a squeeze is going to occur, we will need to see the March return to a premium to the May and preferably also to the July.

Here are the spread charts detailing the change from one of backwardation to a more normal contango situation. When a backwardation structure exists, the spread line will be above zero; when contango exists, the spread will be below zero.

As you can see, the backwardation structure has been easing. At the risk of repeating, if there will be a move to push the shorts during the delivery period in the March next week, this spread line will indicate it by moving back above zero against the May and if it is particularly strong, also against the July contract. I do wish to point out however that while the backwardation structure of the March has eased it is just barely in contango.

Keep in mind that this chart is a snapshot in time and can change so we will need to continue to monitor this for further developments.

To get an even more accurate read on this we would need to capture a snapshot in time comparing the spot silver market bid/offer to the current bid/offer of the nearby March silver contract. At the time I am posting this, spot silver is actually trading about 6 - 7 cents higher than the nearby March futures contract which makes the current structure of the Comex silver market seemingly at odds with the physical market once again. In other words, we have a rather strong backwardation in the physical market but an easing backwardation moving towards contango on the paper market.

An ideal situation for a short squeeze exists when both the futures board and the spot market are speaking with the same voice. In the case of what we have now, if the physical market is as tight as it seems to be, there should be a large number of players standing for delivery in the March. AFter all, if you are a large buyer of silver, and you can get the exact thing by buying a March futures contract at what is a DISCOUNT to the physical market, who in their right mind would not want to do that? If nothing else, a player with the right connections could arbitrage the setup and guarantee an immediate and healthy profit.

Stay tuned on this one. With Silver there is never a dull moment.

March silver's open interest is drawing down rapidly having dropped a bit over 14,000 contracts in yesterday's wild session. There is a decent amount of rolling out of March into May based on the exchange's today, but it is not a one for one roll. Both longs and shorts bailed out yesterday.

There are still a considerable number of contracts open in March, 14,259 to be exact, but we have today's session yet which no doubt will see a further reduction in that contract month.

If a squeeze is going to occur, we will need to see the March return to a premium to the May and preferably also to the July.

Here are the spread charts detailing the change from one of backwardation to a more normal contango situation. When a backwardation structure exists, the spread line will be above zero; when contango exists, the spread will be below zero.

As you can see, the backwardation structure has been easing. At the risk of repeating, if there will be a move to push the shorts during the delivery period in the March next week, this spread line will indicate it by moving back above zero against the May and if it is particularly strong, also against the July contract. I do wish to point out however that while the backwardation structure of the March has eased it is just barely in contango.

Keep in mind that this chart is a snapshot in time and can change so we will need to continue to monitor this for further developments.

To get an even more accurate read on this we would need to capture a snapshot in time comparing the spot silver market bid/offer to the current bid/offer of the nearby March silver contract. At the time I am posting this, spot silver is actually trading about 6 - 7 cents higher than the nearby March futures contract which makes the current structure of the Comex silver market seemingly at odds with the physical market once again. In other words, we have a rather strong backwardation in the physical market but an easing backwardation moving towards contango on the paper market.

An ideal situation for a short squeeze exists when both the futures board and the spot market are speaking with the same voice. In the case of what we have now, if the physical market is as tight as it seems to be, there should be a large number of players standing for delivery in the March. AFter all, if you are a large buyer of silver, and you can get the exact thing by buying a March futures contract at what is a DISCOUNT to the physical market, who in their right mind would not want to do that? If nothing else, a player with the right connections could arbitrage the setup and guarantee an immediate and healthy profit.

Stay tuned on this one. With Silver there is never a dull moment.