Wednesday, March 16, 2011

This is not 2008

I wish to add some additional comments to the previous posts concerning the Japanese Yen, the carry trade and the potential for a QE program commencing by the Bank of Japan as a response to the events in that nation.

There is no doubt that a yen carry trade unwind has been occuring. See my earlier post about this where I discuss the price action of the Yen in comparison to the equity markets in general and the commodity markets.

I noted at the end of that article the following:

"The difference between what happened to commodities and other assets in 2008 was that the Fed was not engaging in any form of QE at the inception of the crisis. It could well be that we now have QE3 set in stone."

A subsequent post then explained my rationale for the Bank of Japan to engage in its own version of Quantitative Easing.

Let me go a bit further here and make a quick case for why this is not 2008 and why we do not need to fear the kind of meltdown in the commodity markets or the equity markets for that matter as occured back then.

First, once the Japanese are able get those nuclear reactors under control, one way or the other, this situation will have been priced in and the markets will reverse higher because that is the nature of markets - they price in the worst case scenario and then once that occurs, it is already discounted and the market then generally moves higher as all the bad news is already accounted for by the then current price level.

In 2008, no one knew the extent to which the tentacles of the derivatives that blew up reached. It was one shoe falling after another. An institution would fail, hope increased that the worst was over and then BLAM, down went another institution. It did not take long for investors to realize that the problem was not going to be dealt with quickly. Indeed, they soon began to understand how intertwined, how pervasive, and complex the problems were. In short, the market feared a near complete collapse of the entire financial system!

Here the situation is known ( an earthquake and the damage associated with it and the subsequent tsunami) and the market is factoring in the worst case scenario of a nuclear meltdown and the effects associated with that. That has forced an avalanche of selling by the hedge funds who are once again proving to be a plague on our financial system by their abuse of leverage. As they unwind that leverage, they sell assets purchased by the use of borrowed money, in this case the yen, (among other currencies including the Dollar to some extent), and then are forced to buy back the yen. If they had learned anything, they might have actually hedged some of these leveraged carry trades by taking some long side protection in the Yen itself but that is another story for another time.

Unlike 2008 therefore, this is not a SYSTEMIC EVENT. It is all connected to the events in Japan and even though it is forcing a yen carry unwind, it may have already run its course because the event, even though it is serious, is a temporary one, which will be resolved. Traders are not peering into some blind unknown as they were back in 2008 because quite frankly, the world had never before in its history seen anything like the "meltdown" associated with these financial weapons of mass destruction. No one knew what to expect and no one knew how it would all end.

Contrast to the events in Japan could not be more evident - while there is a serious knowledge deficit regarding what is actually occuring inside the nation of Japan particularly as it concerns the status of the nuclear reactors, there is a point at which this story will eventually come to a conclusion. In that sense, there is no unknown. The events will play out to their tragic ending leaving thousands of our Japanese brothers and sisters dead, their lives upended and a significant part of their nation in shambles. What will happen however is known - the nation will rebuild and the citizens will pick up the pieces of their lives and go on.

Second - back in 2008 there was no Fed QE and there was no Japan QE. Once the QE was announced by the Fed near the end of 2008, the hemorrhaging stopped and when the program actually commenced in March the next year, gold and the rest of the commodity world took off to the upside. The action by the Fed seemed to take the unknown out of the situation in the one sense that many believed that the Fed would not allow the financial system to utterly fail and when many had believed it would.

My strong belief is that the panic selling we are seeing in the markets is tied not to the earthquake damage or even the tsunami damage but AT THIS POINT to the unknown associated with a nuclear issue. That has jarred confidence and stirred fear and people are selling first and asking questions later.

The truth is the Japanese are going to require massive amounts of raw materials to rebuild their battered infrastructure and that is going to put a firm bid under the base metals and other commodity markets a bit further down the road. The implications are more of a short term bearish thing, long term bullish for commodities in general but particularly bullish for gold because of the implications associated with a QE program by another massive economy. My guess is that as soon as the nuclear issues get resolved, the markets will rebound.

There is no doubt that a yen carry trade unwind has been occuring. See my earlier post about this where I discuss the price action of the Yen in comparison to the equity markets in general and the commodity markets.

I noted at the end of that article the following:

"The difference between what happened to commodities and other assets in 2008 was that the Fed was not engaging in any form of QE at the inception of the crisis. It could well be that we now have QE3 set in stone."

A subsequent post then explained my rationale for the Bank of Japan to engage in its own version of Quantitative Easing.

Let me go a bit further here and make a quick case for why this is not 2008 and why we do not need to fear the kind of meltdown in the commodity markets or the equity markets for that matter as occured back then.

First, once the Japanese are able get those nuclear reactors under control, one way or the other, this situation will have been priced in and the markets will reverse higher because that is the nature of markets - they price in the worst case scenario and then once that occurs, it is already discounted and the market then generally moves higher as all the bad news is already accounted for by the then current price level.

In 2008, no one knew the extent to which the tentacles of the derivatives that blew up reached. It was one shoe falling after another. An institution would fail, hope increased that the worst was over and then BLAM, down went another institution. It did not take long for investors to realize that the problem was not going to be dealt with quickly. Indeed, they soon began to understand how intertwined, how pervasive, and complex the problems were. In short, the market feared a near complete collapse of the entire financial system!

Here the situation is known ( an earthquake and the damage associated with it and the subsequent tsunami) and the market is factoring in the worst case scenario of a nuclear meltdown and the effects associated with that. That has forced an avalanche of selling by the hedge funds who are once again proving to be a plague on our financial system by their abuse of leverage. As they unwind that leverage, they sell assets purchased by the use of borrowed money, in this case the yen, (among other currencies including the Dollar to some extent), and then are forced to buy back the yen. If they had learned anything, they might have actually hedged some of these leveraged carry trades by taking some long side protection in the Yen itself but that is another story for another time.

Unlike 2008 therefore, this is not a SYSTEMIC EVENT. It is all connected to the events in Japan and even though it is forcing a yen carry unwind, it may have already run its course because the event, even though it is serious, is a temporary one, which will be resolved. Traders are not peering into some blind unknown as they were back in 2008 because quite frankly, the world had never before in its history seen anything like the "meltdown" associated with these financial weapons of mass destruction. No one knew what to expect and no one knew how it would all end.

Contrast to the events in Japan could not be more evident - while there is a serious knowledge deficit regarding what is actually occuring inside the nation of Japan particularly as it concerns the status of the nuclear reactors, there is a point at which this story will eventually come to a conclusion. In that sense, there is no unknown. The events will play out to their tragic ending leaving thousands of our Japanese brothers and sisters dead, their lives upended and a significant part of their nation in shambles. What will happen however is known - the nation will rebuild and the citizens will pick up the pieces of their lives and go on.

Second - back in 2008 there was no Fed QE and there was no Japan QE. Once the QE was announced by the Fed near the end of 2008, the hemorrhaging stopped and when the program actually commenced in March the next year, gold and the rest of the commodity world took off to the upside. The action by the Fed seemed to take the unknown out of the situation in the one sense that many believed that the Fed would not allow the financial system to utterly fail and when many had believed it would.

My strong belief is that the panic selling we are seeing in the markets is tied not to the earthquake damage or even the tsunami damage but AT THIS POINT to the unknown associated with a nuclear issue. That has jarred confidence and stirred fear and people are selling first and asking questions later.

The truth is the Japanese are going to require massive amounts of raw materials to rebuild their battered infrastructure and that is going to put a firm bid under the base metals and other commodity markets a bit further down the road. The implications are more of a short term bearish thing, long term bullish for commodities in general but particularly bullish for gold because of the implications associated with a QE program by another massive economy. My guess is that as soon as the nuclear issues get resolved, the markets will rebound.

Additional thoughts on the Yen and the Bank of Japan

There is growing speculation that the Bank of Japan is going to soon start up its own rollout of Quantitative Easing, Phase Two. Some might recall that the very phrase, QE, owes its familiarity to efforts by the BOJ to counteract the deflationary pressures afflicting its economy during the 1990's. In the early part of the next decade, the BOJ, having already reduced interest rates to effectively zero, began buying up its own government debt as well as its agency debt and even equities in an attempt to liquify its economy and stimulate both borrowing and lending. The effort was aimed at securing precisely the same thing that the Fed under Bernanke's leadership is attempting, namely, increasing inflation and inflation expectations to stave off a deflationary mindset.

Regardless of whether one judges that effort successful or not, it is the only viable option left for a Central Bank once it has knocked short term interest rates to zero. After all, the term "zero bound" means something or it means nothing at all. To move further out along the yield curve and reduce interest rates there requires another type of Central Bank "tool" (as Ben Bernanke would term it). That tool is QE.

Given the fact that interest rates in Japan remain chronically low due to the rather tepid rate of economic growth that the nation has been experiencing, the BOJ has really no effective options at this point to attempt to cushion the economy there from the impact of the dreadful earthquake, tsunami and nuclear trifecta which has crushed the nation at a time it could least afford it.

I suspect therefore that the BOJ is going to engage in the same strategy currently being employed by the Federal Reserve here in the US and will shortly announce the commencement of another wave of QE.

This will serve two purposes - or at least it should in theory. First, it will lower longer term interest rates in Japan (not that they were high to begin with) and flood the big banks there with huge sums of cash pumping up reserves and theoretically making lending more affordable for reconstruction purposes. Two - it should serve to undermine the Yen and knock its value down on the global currency markets.

Remember what happened to the US Dollar when the Fed commenced its QE program in March 2009? - it undercut any strength in the greenback that was gained when it experienced a massive rally after the credit crisis erupted in 2008. The Dollar became the go to currency during that time as US stocks and commodities in general were slammed lower jacking up the value of the US currency and slowing down US exports at the very time that policy makers were attempting to generate some sort of economic activity in the US economy. QE put a dagger through the heart of that Dollar rally and has effectively acted to keep a lid on it ever since.

If what I believe is going to happen does, namely a BOJ version of QE, it should tend to depress the value of the Yen which has been bid up to what can only be termed "irrational levels" by panicing speculators unwinding carry trades. The Bank of Japan simply cannot allow the specs to take the Yen any higher without crippling attempts to ameliorate the damage done to the economy there by the earthquake-related tragedy.

Whether or not they actively intervene in the foreign exchange markets this evening or soon thereafter, they are going to attempt to drive the Yen lower.

Once again we get a bird's eye view of history unfolding.

Regardless of whether one judges that effort successful or not, it is the only viable option left for a Central Bank once it has knocked short term interest rates to zero. After all, the term "zero bound" means something or it means nothing at all. To move further out along the yield curve and reduce interest rates there requires another type of Central Bank "tool" (as Ben Bernanke would term it). That tool is QE.

Given the fact that interest rates in Japan remain chronically low due to the rather tepid rate of economic growth that the nation has been experiencing, the BOJ has really no effective options at this point to attempt to cushion the economy there from the impact of the dreadful earthquake, tsunami and nuclear trifecta which has crushed the nation at a time it could least afford it.

I suspect therefore that the BOJ is going to engage in the same strategy currently being employed by the Federal Reserve here in the US and will shortly announce the commencement of another wave of QE.

This will serve two purposes - or at least it should in theory. First, it will lower longer term interest rates in Japan (not that they were high to begin with) and flood the big banks there with huge sums of cash pumping up reserves and theoretically making lending more affordable for reconstruction purposes. Two - it should serve to undermine the Yen and knock its value down on the global currency markets.

Remember what happened to the US Dollar when the Fed commenced its QE program in March 2009? - it undercut any strength in the greenback that was gained when it experienced a massive rally after the credit crisis erupted in 2008. The Dollar became the go to currency during that time as US stocks and commodities in general were slammed lower jacking up the value of the US currency and slowing down US exports at the very time that policy makers were attempting to generate some sort of economic activity in the US economy. QE put a dagger through the heart of that Dollar rally and has effectively acted to keep a lid on it ever since.

If what I believe is going to happen does, namely a BOJ version of QE, it should tend to depress the value of the Yen which has been bid up to what can only be termed "irrational levels" by panicing speculators unwinding carry trades. The Bank of Japan simply cannot allow the specs to take the Yen any higher without crippling attempts to ameliorate the damage done to the economy there by the earthquake-related tragedy.

Whether or not they actively intervene in the foreign exchange markets this evening or soon thereafter, they are going to attempt to drive the Yen lower.

Once again we get a bird's eye view of history unfolding.

Will the Bank of Japan come in to the Forex markets this evening?

That is the big question weighing on the minds of currency traders. The initial knee jerk move higher in the Yen, due mainly in part to repatriation of funds by Japanese companies and citizens to the mainland, can explain the rally in the Yen during the early part of this crisis. However what now appears to be happening is a potential unwind of the Yen carry trade which has been blowing up due to the massive move away from risk. The price action in the Yen compared to the price action of the US equity markets is evidence that many hedge funds have been borrowing Yen and then using that cheap money to leverage up on US stocks. While the carry trade using this particular currency is no where near the size it was back in 2008, it is still very large. Back in 2008 when the credit crisis erupted in the US and spread around the globe, the Yen staged an enormous rally.

Hedge funds, which had acquired massive leveraged positions using the Yen as the funding currency, commenced a headlong rush to the exits en masse. In effect they had acquired a massive short Yen position which the Japanese monetary authorities were more than happy to condone. When the Yen began moving higher, suddenly the trade began souring as gains in the leveraged positions were being dragged underwater by losses on the currency front due to gains in the funding currency. As commodities and stocks were sold off, the trade because to collapse. Their panic to deleverage forced the Yen sharply higher even as the stock markets and commodity markets were obliterated to the downside.

Once again we can see what what appears to be an exact repeat of late 2008. Given the fact that the Japanese economy has been devastated by recent events, the last thing that the Japanese monetary authorities want to see is a soaring yen, which will effectively cut off their export markets at the knees by hurting their price competitiveness on the global markets.

What we might see begin to happen is the BOJ coming in and beating the fire out of the speculators by selling enormous amounts of Yen on the foreign exchange markets this evening or very soon. One wonders what they might do with all the US Dollars that such action would accumulate in their coffers. In the past they would sterilize the intervention effort by purchasing US Treasuries.

If that were to happen this time around, the Fed could sit back and watch the BOJ do its QE work for it.

Again, this situation is very fluid and can turn on a dime but it is highly unlikely that the BOJ and the Japanese Ministry of Finance are not keenly watching what the hedge funds are doing to its currency.

The difference between what happened to commodities and other assets in 2008 was that the Fed was not engaging in any form of QE at the inception of the crisis. It could well be that we now have QE3 set in stone.

Hedge funds, which had acquired massive leveraged positions using the Yen as the funding currency, commenced a headlong rush to the exits en masse. In effect they had acquired a massive short Yen position which the Japanese monetary authorities were more than happy to condone. When the Yen began moving higher, suddenly the trade began souring as gains in the leveraged positions were being dragged underwater by losses on the currency front due to gains in the funding currency. As commodities and stocks were sold off, the trade because to collapse. Their panic to deleverage forced the Yen sharply higher even as the stock markets and commodity markets were obliterated to the downside.

Once again we can see what what appears to be an exact repeat of late 2008. Given the fact that the Japanese economy has been devastated by recent events, the last thing that the Japanese monetary authorities want to see is a soaring yen, which will effectively cut off their export markets at the knees by hurting their price competitiveness on the global markets.

What we might see begin to happen is the BOJ coming in and beating the fire out of the speculators by selling enormous amounts of Yen on the foreign exchange markets this evening or very soon. One wonders what they might do with all the US Dollars that such action would accumulate in their coffers. In the past they would sterilize the intervention effort by purchasing US Treasuries.

If that were to happen this time around, the Fed could sit back and watch the BOJ do its QE work for it.

Again, this situation is very fluid and can turn on a dime but it is highly unlikely that the BOJ and the Japanese Ministry of Finance are not keenly watching what the hedge funds are doing to its currency.

The difference between what happened to commodities and other assets in 2008 was that the Fed was not engaging in any form of QE at the inception of the crisis. It could well be that we now have QE3 set in stone.

4 Hour Silver Chart - update

More volatility - more wild and unpredictable price swings. Most of the markets are now trading the news out of Japan regarding the nuclear reactors. Price is shooting higher and then collapsing based on what the news is.

The only thing that immediately matters is the reactor situation.

The only thing that immediately matters is the reactor situation.

Copper finding support near $4.10

With all the volatility in the markets right now, attempting to read too much into a single day's trading activity is foolish. That being said, it is noteworthy that copper is moving higher on a day in which we get the news that US Housing starts fell in the month of February to the lowest level since April 2009. If that was not bad enough, building permits also dropped to a record low.

The problem in the US is the obvious glut of foreclosed homes and distressed home sales not to mention the poor labor markets and tougher credit standards.

Then why is copper moving higher especially on a day in which the equity markets are getting crushed lower out of fears over slowing global growth?

One possible explanation is that some traders are perhaps looking past the current and real slowdown fears and focusing on what they believe will be massive buys by the Japanese as they attempt to rebuild their shattered nation once they can somehow get the nuclear issue resolved. They are going to need enormous amounts of raw materials to rebuild parts of the nation which look to have been swept with a broom of destruction.

Stay tuned.

The problem in the US is the obvious glut of foreclosed homes and distressed home sales not to mention the poor labor markets and tougher credit standards.

Then why is copper moving higher especially on a day in which the equity markets are getting crushed lower out of fears over slowing global growth?

One possible explanation is that some traders are perhaps looking past the current and real slowdown fears and focusing on what they believe will be massive buys by the Japanese as they attempt to rebuild their shattered nation once they can somehow get the nuclear issue resolved. They are going to need enormous amounts of raw materials to rebuild parts of the nation which look to have been swept with a broom of destruction.

Stay tuned.

Silver experiences sharp jump in EFP activity yesterday

Data released by the CME Group this morning detailing changes in open interest and volume readings from yesterday's trading session showed a rather substantial jump in what are known as Privately Negotiated Transactions. They are also generally known as Exchange for Physical or EFP's.

I have been monitoring this data for about a month now especially as silver was going into its delivery process for the March contract.

While one day a trend does not make, yesterday recorded a sharp increase in these off exchange type agreements but it was for the May contract and not the March. There were 5,934 of these conducted yesterday.

To give you a bit of perspective - over the last month, the daily average of these transactions has been 1,433 for the May.

With rumors abounding in the silver market about shorts offering longs cash payments at a substantial premium above the current board price in lieu of standing for delivery of the physical metal, perhaps there is something to this. I would have expected this sort of activity to be showing up in the March contract however and not so much in the May at this point. At this point do not read too much into this but just note the occurence.

In the actual delivery process for the March contract, a total of 847 have been done at this point in the month with 1,079 contracts still open in that month. So far I have not seen anything that really stands out to me about these deliveries. The Bank of Nova Scotia and JP Morgan have been the largest issuers or those delivering the silver while Barclay's has been the largest stopper or the one taking the silver.

I should note that Morgan's deliveries are mainly for customers and not for the house at this point.

I will want to see tomorrow's data and preferably the rest of the week's before jumping to any conclusions however. The fact that the March contract cannot get to the sharp premium to the May contradicts both the rumors that are abounding and the jump in EFP volume.

Needless to say to the old timers - this is silver - always full of rumors and always a big mystery. It has been that way for as long as I can remember.

I have been monitoring this data for about a month now especially as silver was going into its delivery process for the March contract.

While one day a trend does not make, yesterday recorded a sharp increase in these off exchange type agreements but it was for the May contract and not the March. There were 5,934 of these conducted yesterday.

To give you a bit of perspective - over the last month, the daily average of these transactions has been 1,433 for the May.

With rumors abounding in the silver market about shorts offering longs cash payments at a substantial premium above the current board price in lieu of standing for delivery of the physical metal, perhaps there is something to this. I would have expected this sort of activity to be showing up in the March contract however and not so much in the May at this point. At this point do not read too much into this but just note the occurence.

In the actual delivery process for the March contract, a total of 847 have been done at this point in the month with 1,079 contracts still open in that month. So far I have not seen anything that really stands out to me about these deliveries. The Bank of Nova Scotia and JP Morgan have been the largest issuers or those delivering the silver while Barclay's has been the largest stopper or the one taking the silver.

I should note that Morgan's deliveries are mainly for customers and not for the house at this point.

I will want to see tomorrow's data and preferably the rest of the week's before jumping to any conclusions however. The fact that the March contract cannot get to the sharp premium to the May contradicts both the rumors that are abounding and the jump in EFP volume.

Needless to say to the old timers - this is silver - always full of rumors and always a big mystery. It has been that way for as long as I can remember.

Food Inflation now showing up even in official statistics

We have been saying for months now that there is a lag between the time that prices in the actual economy respond to changes in the prices reflected in the futures markets. While the CCI, the Continuous Commodity Index, has been knocked down rather rudely in the last few trading sessions as hedge fund money has flowed out of the sector due to risk aversion, it is still at extremely high levels. Even given the recent carnage inflicted to the commodity sector, the CCI has only dropped back to levels it had attained in January of this year. In other words, while prices have come off some, they are still elevated.

In my experience there is generally a lag of about 4 months or so before the prices being reflected in some of the futures markets impact the wider economy as a whole, particularly the retail level. With this in mind, please note the following headline that came out this morning.

The Labor Department said Wednesday that the Producer Price Index rose a seasonally adjusted 1.6 percent in February -- double the 0.8 percent rise in the previous month. Outside of food and energy costs, the core index ticked up 0.2 percent, less than January's 0.5 percent rise.

You can read the entire story here:

http://finance.yahoo.com/news/Wholesale-prices-up-16-pct-on-apf-3777454020.html?x=0&.v=1

In my experience there is generally a lag of about 4 months or so before the prices being reflected in some of the futures markets impact the wider economy as a whole, particularly the retail level. With this in mind, please note the following headline that came out this morning.

Wholesale prices up 1.6 pct. on steep rise in food

Wholesale prices rise 1.6 pct. due to biggest jump in food costs in more than 36 years

On Wednesday March 16, 2011, 8:57 am EDT

WASHINGTON (AP) -- Wholesale prices jumped last month by the most in nearly two years due to higher energy costs and the steepest rise in food prices in 36 years. Excluding those volatile categories, inflation was tame.The Labor Department said Wednesday that the Producer Price Index rose a seasonally adjusted 1.6 percent in February -- double the 0.8 percent rise in the previous month. Outside of food and energy costs, the core index ticked up 0.2 percent, less than January's 0.5 percent rise.

You can read the entire story here:

http://finance.yahoo.com/news/Wholesale-prices-up-16-pct-on-apf-3777454020.html?x=0&.v=1

4 Hour Gold Chart

Gold is finding buying support in today's session after its bounce off of strong support near $1380. It has run back to former support now turned resistance near $1405 which is serving to hold it in check for now.

Bulls need a push through this level to move back towards $1420.

Volume is also so-so reflecting the indecision and uncertainty that still exists in traders' minds.

Bulls need a push through this level to move back towards $1420.

Volume is also so-so reflecting the indecision and uncertainty that still exists in traders' minds.

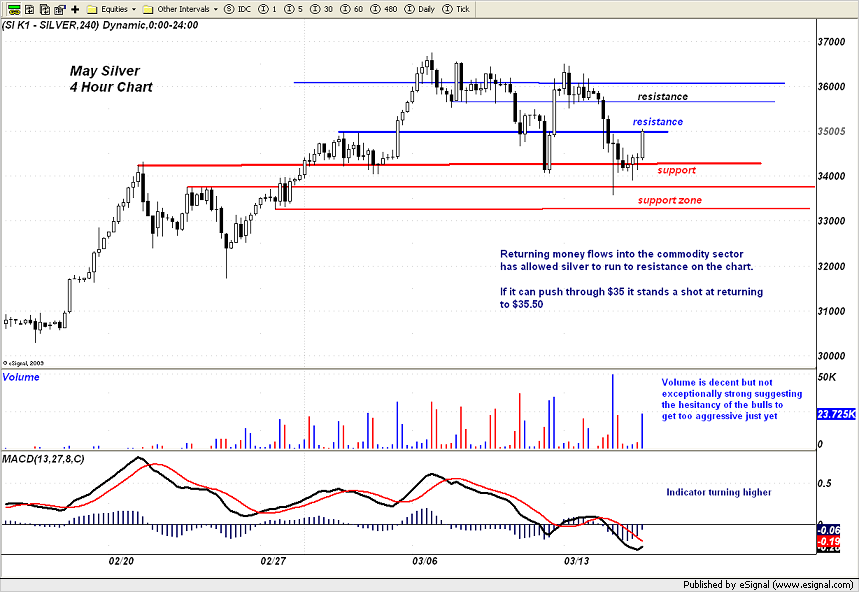

Commodity Complex back in Favor Today

Money flows have returned to the Commodity Complex today which is a bit unusual considering that the stock market cannot seem to move all that much higher. It is not as though risk is back in therefore and risk aversion has gone away for the day. Just look at the bond market which still is moving higher and the Dollar which has gotten the usual little blip related to safe haven plays.

Perhaps traders felt as if the selling in the commodity sector was overdone. Either way it is allowing silver to move up more than 2% at this time and gold to return above $1400.

Crude oil is higher also due to events in Bahrain with traders focusing on potential supply disruptions today and not demand destruction as they have been doing in recent days.

Perhaps traders felt as if the selling in the commodity sector was overdone. Either way it is allowing silver to move up more than 2% at this time and gold to return above $1400.

Crude oil is higher also due to events in Bahrain with traders focusing on potential supply disruptions today and not demand destruction as they have been doing in recent days.